Crouching Biden, Hidden Bailout

The art of the steal

If there’s one lesson that the capitalist class actually learned from 2008, it’s that people don’t like bailouts. You bail out too hard and too visibly, and you get the movement of the squares, smelly Occupy Wall Street weirdos come and yell at you during your mimosa brunches, which is rather unpleasant. And that’s why, despite the fact that the last week has seen one of the largest government bail outs of the banking sector in history, the government response to the financial crisis has barely scratched the surface of the daily news.

The Biden administration stepped in over the weekend to “guarantee” all depositors at Silicon Valley Bank (SVB), even the uninsured ones, will be able to get their money from the Fed. This was designed to stop a spreading bank run, in which depositors from dozens of banks would suddenly withdraw their cash, spooked by the sudden collapse of SVB and thereby causing the collapse of many more. But, as happened inevitably, the treasury soon announced that the depositor back up would also apply to the other two failed banks, Signature and Silvergate. It doesn’t take a specialist in pattern recognition to realize that the administration was de-facto insuring all deposits at every bank in the country.

So on Wednesday Treasury Secretary Janet Yellen held a press conference to try and deny this quite obvious fact, and said that they are not going to guarantee all uninsured deposits—only the uninsured deposits of those banks whose failure would create “systemic risk”. In 2010, the Dodd-Frank act named a number of banks “systemically important financial institutions” (SIFI), which was an attempt to get people to stop saying Too Big To Fail, but which also instituted greater regulation and scrutiny on those banks.

But Yellen was not using that technical definition, which includes only the top 30 global banks, instead she defined it to mean literally any bank over a $150 billion market cap, which means it’s basically all the big banks and all the mid-sized regional banks, but local and community banks are on their fucking own. Unsurprisingly, community banks are nervously declaring that they’re doing fine, actually, because it is incredibly likely that all their biggest deposits will flee for safer territory (and indeed, Bank of America is doing incredible deposit business this week, as companies and rich scum flee as fast as they can into the arms of the Too Big or even Too Mid to fail.)

Now, as a reminder, the FDIC already insures any deposits up to 250,000, or, in other words, all the bank accounts of anyone who isn’t literally a rich person or a medium-sized business. So when Biden says “Americans will not lose their deposits”, he doesn’t mean you and me, who were never in danger of this, because we have so little money that our poverty is not and has never been a question the government feels impelled to address.

But again, these “deposit backstops” look an awful lot like, well, bail outs. Biden insists that they are not using taxpayer money to help the banks, only FDIC funds paid into by banks. They’re just “helping depositors”, a cute phrase which hides the fact that these poor imperiled depositors include, EG, Peter Thiel.

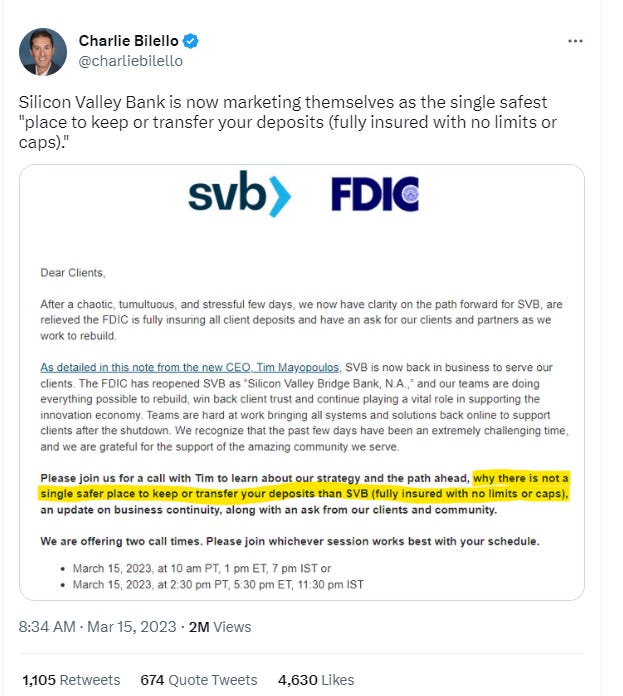

And what has this “deposit” “backstop” (not a bailout!) meant? Well, Silicon Valley Bank, in an act of defiant assholery reminiscent of 2008, sent out an email advertising their bank as the safest place to make deposits.

This is the very definition of “moral hazard”, a phrase capitalists like to use to describe giving people free healthcare or unemployment insurance since it “incenitivizes” them toward laziness, but hate when you use it in its proper context, which is the way that government policy incentivizes banks to not give a flying fuck about anything because they know Uncle Sam is gonna cover their losses when they wake up on the floor of their casino hotel room with empty pockets and a loud insistent knocking at the door.

Similarly, First Republic, the next US bank on the chopping block whose stock price has utterly imploded over the last week, received a non-bail out bail out yesterday in the form of 11 of the big banks—BoA, JP Morgan, etc—agreeing to make 30 billion dollars of cash in ‘uninsured’ deposits into First Republic. This sudden act of capitalist mutual aid emerged after Jamie Dimon, chief ghoul of Chase, met with secretary Yellen on Friday.

It is widely believed on the street that the Fed has in fact agreed to backstop those 30 billion in “uninsured” deposits, so it’s actually a no-risk situation for the bankers. If the bank collapses, the treasury will pick up the bill of these noble white knights who get a PR boost for looking out for the sector’s health. This utterly transparent act of confident boosting is boosting no one’s confidence, as stocks and futures rallied briefly yesterday before continuing their plunge, and First Republic is back on its trajectory to bankruptcy, its stock price dropping another 20% before stock openings Friday.

This is tautology magic, pure cope and magical thinking in the form of billions of dollars of cash distribution. Think about it: if this kind of deposit backstopping works, and keeps further banks from failing, it can only do so because, in fact, the bank failures were part of a totally isolated, non-structural and idiosyncratic set of conditions, particular to each bank. If that’s the case, then the backstop was actually unnecessary, since the failure of the bank wouldn’t have been a problem anyway. However, if there is structural risk and underlying financial crisis, then backstopping depositors wont do anything, because the failures are deeper than just these banks, and, again, the cash is just being given away to the fuckers lucky enough to be invested in the most poorly managed banks.

In other words, these backstops do nothing to solve any of the problems except the magical problem of “confidence”; the most expensive comfort blankets in the world.

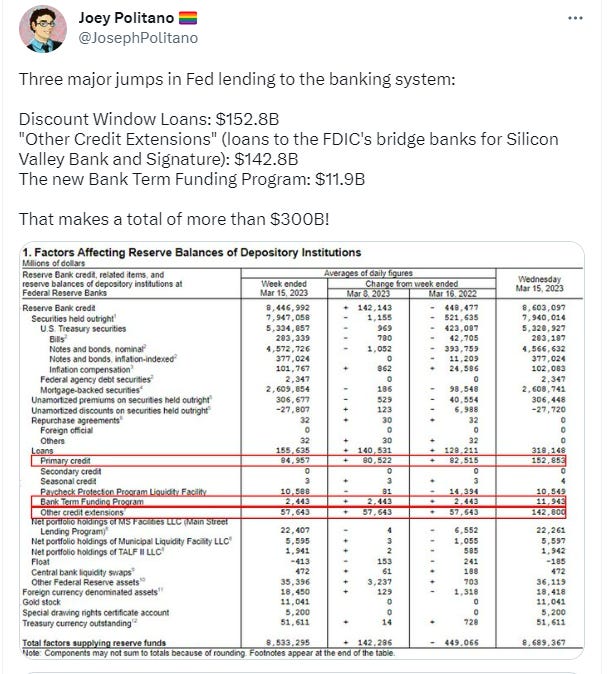

But the thing is, these big visible moves are in fact just the magician’s flourish, the prestige. Because the real meaty bail outs are happening behind the scenes. In an announcement noted very carefully by bankers but not the public, the Fed’s “discount window”, a special fund giving very low-interest cash loans to institutions in crisis, opened wide over the weekend. While the public facing finance news networks talk about inflation, the coming Fed meeting and whether the rate hike will be .25 or .5, the fed has been shoveling free money out the discount window, to the tune of 152 billion dollars. Combined with their bridge loans to SVB and Signature and the new Fed program, the Fed has lent over $300 billion in the last week to the finance industry. Sorta looks like a bail out, huh?

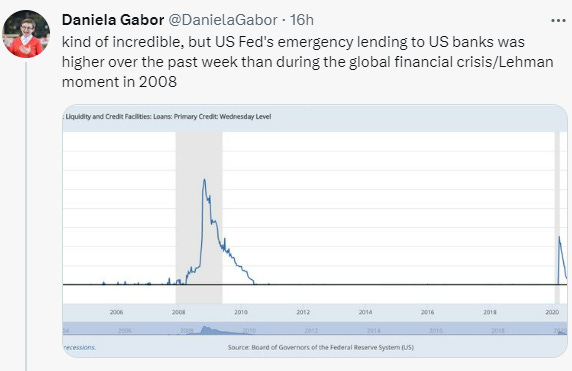

In fact, the Fed’s emergency lending has ALREADY been bigger than the lending in 2008, and that’s before anything “truly structural” has happened.

The hacks want to reassure us that the lessons have been learned from 2008, that the banking system is much stronger than it used to be, that regulation has been much better. Please ignore the doomsayers who are saying that Credit Suisse (the European bank teetering on the edge of oblivion this week, and one of the largest banks in history, which has received its own massive bail outs from the Swiss National Bank) might be Too Big to Save.

But it’s vitally important that we not be confused: there are bail outs going on, massive bail outs, and that’s before the rubber has really hit the road. The government is fucking SPOOKED, everyone in DC is scared shitless, and they really want us to believe that this crisis is contained, that their fast action staunched the bleeding made by a couple irresponsible actors who were over concentrated in particular sectors. Maybe they’re right. Maybe the worst is over. But SVB didn’t just have VC money, it was also deeply invested in YIMBY “affordable housing”. And the commercial rents sector still hasn’t recovered from the damage done to office spaces by hybrid and work from home. And if real estate is in crisis, well, let’s just say I’m not holding my breath.