RIP Neoliberalism

Wile E Coyote looks down

Special Shout Out to Mia Wong, with whom I developed these ideas by texting jokes back and forth and who gave me the first sentence of the essay.

The long 2016 is finally over. With the collapse of Silicon Valley Bank (and high tech and crypto finance in general) we are in for a general financial collapse which sure looks to be The Big One. Great Depression 2: Make America Great(ly depressed) Again. It is only appropriate that the collapse would start in tech—just as everyone suspected it would—but crypto currency as first-domino to fall is truly hilarious, the second funniest scenario (behind only 2020 rioters destroying the Mall of America and thereby causing a cascading commercial-rents collapse).

Despite the loud insistence from Biden, financial commentators and their various supporters on social media that this collapse is in fact contained to Silicon Valley, every now and then the truth slips out of mouths too used to simply praising Caesar. The Fed’s Sunday night statement “This is NOT 2008” has a lot of people asking questions already answered by their Sunday night statement. And when Biden says “there is no contagion”—a claim he’s spent his administration making about an altogether different kind of epidemic—its pretty hard to take it at all seriously.

Biden was of course part of the Obama admin as it kicked the can of the 2008 crisis down the road. It has been a miraculous series of lucky breaks, labor busting (app economy), financial deregulation (regional banking) and wealth extraction (rent increases)—combined of course with China more or less paving its entire South East Coast—that has kept the bill from coming due for 15 years. In one of the most fantastic acts of spectacular management, the capitalist class bought itself more time than even its economist priests believed possible, almost completely divorcing finance from the real economy.

But as the capitalists always do, they got high on their own supply and forgot that the whole thing was built on Obama’s blank check. One wing of capitalists, including agribusinessmen, arms dealers, oil drillers, landlords and mega-retailers, more honest to the political moment, full of resentment at their perceived political marginalization and that Obama’s bailout didn’t help them (their corn subsidies and government funded pipelines don’t count!), whipped the exurban white petit bourgeoisie into a frenzy of hate and confusion.

Another wing believed it was their entrepreneurial genius that made this seemingly magical rentier economy keep producing profit, preaching “disruption” “knowledge” “learning” and “moving fast and breaking things”. The most delusional of them began to believe that the question of value had been solved at last, as cryptocurrency could somehow magically turn code and electricity into endless value.

In the meantime, social movement exploded across the globe. But where previous waves of struggle saw partial recuperation and concession, this wave saw only the most symbolic concessions—Nancy Pelosi in a daishiki took a knee—while protestors got their heads bashed and their lungs filled first tear gas then Coronavirus. The thing about a bill is it does come due, and the political price to be paid for the last fifteen years may indeed end with capitalists strung up from lampposts.

The Bank Run

Events are moving very quickly, but as of Monday morning, three banks have collapsed, two of them (Signature and Silvergate) largely focused on turning Cryptocurrency into cash, but the third, Silicon Valley Bank, the 14th largest bank in America, was largely the home for the vast majority of bay area venture capital, giving tens of millions of dollars in loans to tech start up funds that promised to make the next great peanut and butter jelly sandwich.

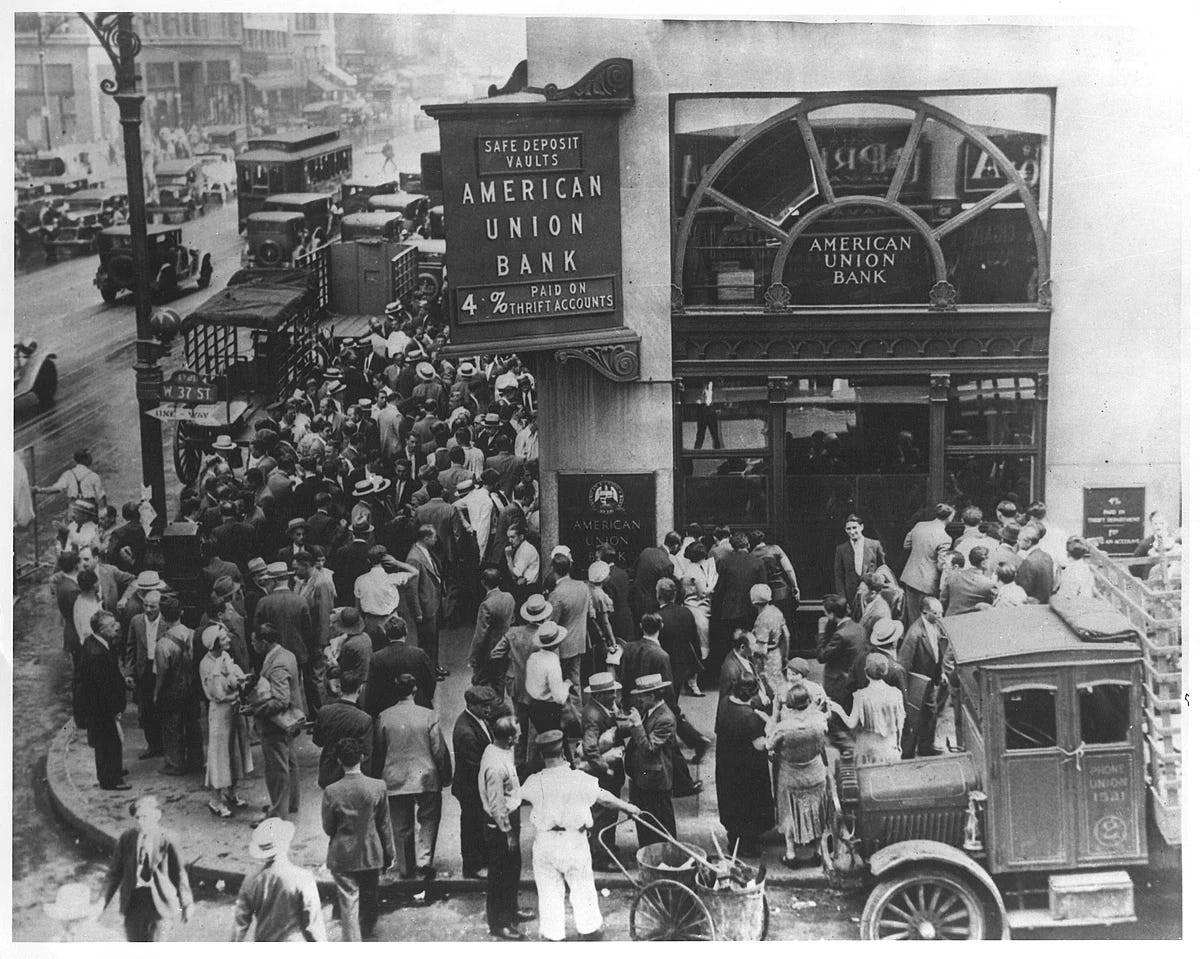

On Monday of last week, March 6th, Silvergate—a bank almost exclusively in the cyrpto business—declared insolvency. On Wednesday the 8th Silicon Valley Bank (SVB) announced that it was looking for a whopping amount of cash—maybe even a buyout--to stay in business. This led to a huge chunk of their customers withdrawing as much cash as they could get—a classic bank run, in which confidence in the bank suddenly collapses, and everyone moves to withdraw their money, which reveals that in fact the bank doesn’t have enough money on hand to pay out all its deposits (they never do, their job is to invest and create debt), and they are forced into bankruptcy. If this is sounding familiar from what you learned in high school education about the Great Depression, well, yeah.

But didn’t the federal government intervene to make sure this kind of bank run couldn’t happen again? Yes, to small depositors. The FDIC guarantees all deposits up to $250,000 in case of bankruptcy, which means that the vast majority of us will never truly be threatened by this particular scenario happening to our, lol, “savings”. But corporate customers—in the case of SVB mostly tech entrepreneurs and venture capitalists—leave much more than 250k in the bank, and suddenly on Friday it appeared hundreds of companies wouldn’t even be able to make payroll.

In a shocking show of capacity, the Biden administration moved fast, announcing on Sunday night they would make further FDIC funds available for depositors at SVB and Silvergate, a “backstop” which was meant to restore confidence in the financial sector. That confidence didn’t even last to the opening bell Monday morning. News that First Republic Bank had asked for tens of billions of dollars from the fed led its stock into total freefall, losing 60 percent of its value in pre-market trading, and with it the rest of the Dow. (Update: as of 1030 AM, a trading halt has been placed on 30 banks).

Biden insists that this isn’t a bailout—after all, they’re only repaying depositors (aka: silicon valley venture firms) and not the shareholders (similar if not the same silicon valley firms). The Biden administration’s greatest public relations talent is making distinctions without a difference that fool nobody. We had to go back to work and die of Covid rather than get a single inch of extra benefits and support, but tech bros who invested millions of dollars in Scaffx, the crowdsourced app that shows you where scaffolding is set up in your town, only had to whine on twitter for 36 hours before getting all their money back.

But the backstop didn’t help, and it doesn’t matter, because the problem is a hell of a lot deeper than crypto or even tech venture firms. In a series of hilarious revelations, it turns out that SVB didn’t even have a chief risk officer for most of 2022, and that Joseph Gentile, Chief Administrative Officer at SVB securities, was CFO for Lehman Brother’s. But while SVB may be the most incompetent, they are also only one part of a massive trend.

You can only divorce the financial sector from the real economy for so long before the bare sharp facts of value—which can, in the final analysis, only be extracted from workers, ‘nature’, the colonized and the dispossessed—pop the bubble. The collapse we’ve all seen coming for years is here.

However, we must not say this, because if we say it, it will become true. In moments of crisis the economists rely on the coddest of cod psychology—banking runs are just panics, just a question of attitudes and opinions. So if everyone stays levelheaded, the collapse wont happen, because, after all, the market is just a social fiction produced between traders, bankers and experts. This lie, that even mentioning the situation will create the panic, is just a stalling tactic to give the top of the capitalist class enough time to maneuver what cash they can into safe havens before the bottom truly falls out.

But if declaring a crisis which only really started last Wednesday over by Sunday night seems absurdly premature, it’s because the capitalist class has been declaring this crisis over prematurely since 2009—hell, since 1973. When all you have is a hammer…

The Balance of Forces

In a stirring press conference Monday morning, Biden announced that, since the crisis was now contained, he would be doing more banking regulation. You could describe it with the delightfully sapphic cliché of putting a finger in the dike but it’s not even that, he’s just threatening to put a finger in the dike. Even if there was a bill to impose new banking regulations on his desk today it wouldn’t make a lick of difference, but the famously helpful and compliant house Republicans are on a week long policy retreat anyway, so there’s literally nothing congress can even begin to do until next Monday. Too little too late is too optimistic an analysis.

The political solution to the massive bank collapse of 2008 was to bailout the too big to fail banks, and tell the rest of us to fuck off. “Banks got bailed out, we got sold out” as I remember chanting a whole hell of a lot in 2011. As we lost homes to underwater mortgages, rents skyrocketed putting millions of us on the street, gentrification exploded and VC-funded tech disruptors undercut our wages, the Democrats insisted on normality while the Republicans goose-stepped across the hinterland.

We were very partially pacified by web tech, social media, streaming and the explosion of alienated but in undeniable ways incredible technologies that came to define almost every waking moment of our lives. Meanwhile our student and medical debt ballooned, which universities, insurance industries and hospitals used to consolidate and capture ever greater land holdings in newly desirable urban areas. The government gave us platitudes, and, every four years, an opportunity to pretend to staunch the fascist creep. Most importantly, the housing market, decimated by 2008, got back on its feet and once again began robbing us of all our wages.

But this pattern of debt instead of actual concessions, papering over increasing costs of living in the imperial heartland by easy credit that could buy things kept cheap by spreading logistics networks and sweatshops across the globe, all paid for by cutting social services and privatizing everything, goes all the way back to the seventies. Credit cards caused the Savings and Loan crisis in the 80s, investment, pension and 401k manipulation the dot com burst, housing debt 2008. But now we are all basically squeezed for every ounce of debt-driven productivity we can take.

Obama (and Biden) could’ve won decades of social peace if, in 2007/8, they had practiced mortgage and student loan forgiveness and instituted Medicare for All. Obamarcare is instead a perfect symbol of putting off the inevitable. It expanded health care and temporarily reduced costs for enough people that it eased the political pressure, while putting in place funding and rating systems that lead to the massive consolidation of super-hospital-systems with the administrative capacity to fulfill all the investigation and information reporting requirements Obamacare introduced through its competitive funding models. Obamacare gave with one hand while taking away with the other: more people were technically covered by health insurance marketplaces while at the same time (already underserved) rural and even suburban health systems got gobbled up, gutted for parts and otherwise streamlined or destroyed.

But the problem with an incentivized competitive funding model, in which your ranking determines how much federal assistance you receive, is that eventually all the non-competers are simply forced out of business. And if, say, a pandemic hits…

Much as they handled healthcare by putting off the day of reckoning, so did they handle the financial collapse. Trillions in cash saved 2008 from looking like a Great Depression, but it also taught bankers that they were too big to fail. Indeed, it seems clear that the mortgage-backed securities products that were at the heart of the 2008 bubble have just been reorganized and rebuilt as rent-backed securities: in other words, our rents keep going up because finance needs to keep the ponzi scheme running. It is little talked about in the flurry of news stories, but SVB in 2022 had basically no investment in housing backed securities, but by the beginning of 2023 was the number one regional bank in terms of housing investment. In other words, the banking industry is still treating the housing market as a safe haven for profit, as a line that only goes up. The demise of SVB doesn’t just reflect entrepreneurial and tech failure, it represents the end of the housing market backstop.

But still the Democrats had political opportunities to recapture the initiative. The great mistake the liberals made was to knife Bernie Sanders in 2019. Had they gone with Sanders, the political recuperation of movement energy would almost certainly have dampened the broad base of support and movement in 2020, and would have built a strong right flank within the left that could head-off any future movement. Not to mention if Sanders had instantiated Medicare for All, it might have built a semi-permanent political coalition like the one in the UK that kept Labor in power for three and a half decades after the war.

But instead, we got more can kicking, with a return to Biden and in particular the sociological production of the “end of the pandemic” (see Death Panel podcast for more about this). History will remember this as one of the most horrifying and violent failures in public health history, but at least we got back to work in time to see all our savings wiped out by the financial crisis.

I belabor all these Democratic errors to point out that, if we are indeed entering another Great Depression, the only part of the capitalist class with a strong connection outside of the establishment is almost all far right. This means that liberals are terribly positioned for the struggle that is almost sure to come. There is no FDR to save that coalition. The liberals have bought fifteen years of capitalist restructuring in exchange for their historical role in heading off serious political transformation.

It is only appropriate that Neoliberalism’s death throes should be triggered by a 320 pixel jpeg of an ape smoking a pipe. Such a legacy of violence and cruelty deserves such a banal and ugly headstone. As the current financial order collapses, there will be untold suffering that will demand a response similarly unimaginable. We have learned through this pandemic that there is no one who is going to help us, no one coming to save us. But the liberals have taken themselves off the board and the initiative is ours to use. If we can really use the skills in struggle, mutual aid and community building we have developed over the last fifteen years, I believe we will have an opportunity to make this crisis capitalism’s last.